BACKGROUND

IAS 29, Financial reporting in hyperinflationary economies applies when an entity’s functional currency is ‘hyperinflationary’.

IAS 29 requires the financial statements (including any comparative periods) to be stated in terms of the measuring unit current at the end of the applicable reporting period. This is because the currency of a hyperinflationary economy loses a significant amount of purchasing power from period to period such that presenting financial information based on historical amounts, even if only a few months old, does not provide relevant information to users of financial statement.

ACCOUNTING IMPACT

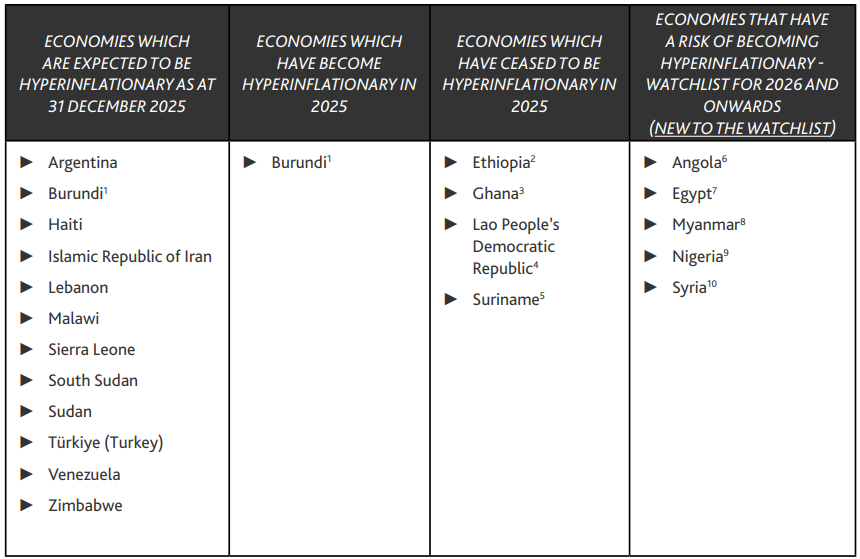

With increasing inflation rates and declining economic conditions around the world, many jurisdictions remain on the watchlist, however, four jurisdictions have ceased to be hyperinflationary in 2025 – Ethiopia, Ghana, Lao People’s Democratic Republic and Suriname

The term ‘hyperinflation’ is not defined in IAS 29, as it is a matter of judgment. IAS 29 provides the following example characteristics of a hyperinflationary economy (IAS 29.3):

(a)the general population prefers to keep its wealth in non-monetary assets or in a relatively stable foreign currency. Amounts of local currency held are immediately invested to maintain purchasing power;

(b)the general population regards monetary amounts not in terms of the local currency but in terms of a relatively stable foreign currency. Prices may be quoted in that currency;

(c)sales and purchases on credit take place at prices that compensate for the expected loss of purchasing power during the credit period, even if the period is short;

(d)interest rates, wages and prices are linked to a price index; and

(e)the cumulative inflation rate over three years is approaching, or exceeds, 100%.

The International Monetary Fund (IMF) publishes historical and projected inflation data by country.

In July 2025, the IFRS Interpretations Committee (the Committee) published an agenda decision titled Assessing Indicators of Hyperinflationary Economies. The request asked a number of questions about assessing whether an economy is hyperinflationary, such as whether all indicators in IAS 29.3 should be considered in assessing when an economy becomes hyperinflationary, including whether to continue to consider all indicators even when one indicator in IAS 29.3 has been met. Evidence gathered by the Committee indicated little, if any, diversity in understanding the requirements for assessing when an economy becomes hyperinflationary. According to the evidence gathered, stakeholders do not conclude that an economy becomes hyperinflationary based solely on one of the indicators listed in IAS 29.3, such as the cumulative inflation rate.

During 2025, the list of hyperinflationary economies (and those economies on our watchlist) has continued to evolve due to deteriorating economic conditions and high inflation in several countries. The jurisdictions on the list of hyperinflationary economies must apply IAS 29, which results in financial statements (both current and prior comparative periods) being restated to reflect current inflation rates.

Based on the IMF’s October 2025 World Economic Outlook (IMF WEO), below is an updated snapshot of countries which are expected to be hyperinflationary as at 31 December 2025, countries which have become hyperinflationary (or have ceased to be hyperinflationary) during 2025, and countries which are at risk of becoming hyperinflationary in 2026.