Introduction

This How-to guide was produced as part of a joint know-how initiative between Cosegic Limited and Lexology Pro.

This guide will assist in-house counsel, private practice lawyers, and risk and compliance professionals to understand the requirements and scope of the Financial Conduct Authority’s (FCA) Consumer Duty (Duty).

This includes consideration of the package of measures comprising new Principle 12 which requires firms to ‘act to deliver good outcomes for retail customers’ alongside the obligations imposed on firms by the three cross-cutting rules and the key elements of the firm–consumer relationship to deliver good outcomes. In-scope firms should also note new Individual Conduct Rule 6 which requires employees to act to deliver good outcomes for retail customers.

Challenges associated with monitoring data, meeting customers’ needs (including vulnerable customers and conducting fair value assessments) as firms embed the Consumer Duty into their culture and how best to deal with these, are explored in more detail.

This guide covers:

- The main elements of the Consumer Duty

- Delivering good consumer outcomes

- Practical steps to post-implementation compliance

This guide can be used in conjunction with the following Checklist: Embedding the Consumer Duty: practical considerations.

Section 1 – The main elements of the Consumer Duty

The Consumer Duty was implemented by the FCA to set higher and clearer standards of consumer protection across financial services to put customers’ needs first. This has been described as a major shift in the UK financial services’ regulatory landscape, and this is particularly relevant as consumers face increasing pressures, including those relating to the cost of living.

1.1 Rules and guidance

The FCA published final non-handbook guidance for firms (FG22/5) and a policy statement (PS22/9) for the new Consumer Duty on 27 July 2022. This follows consultations which had been published in May 2021 (CP21/13) and December 2021 (CP21/36) to shape the structure of the new framework.

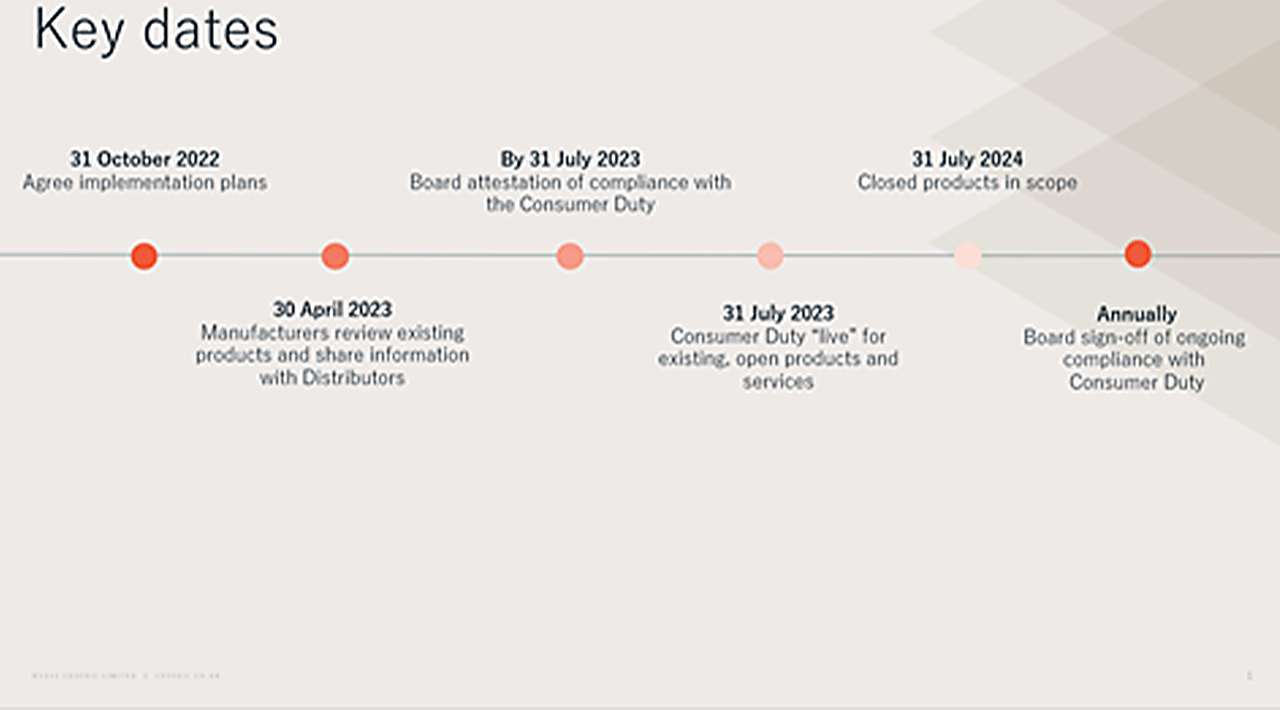

Given the extent of planning involved, the FCA introduced a phased approach to implementation. For new and existing products or services that are open to sale or renewal, the rules came into force on 31 July 2023. For closed products or services, the rules came into force on 31 July 2024.

The rules build on the existing FCA Handbook requirements aimed at mitigating harm to consumers as well as obligations under general consumer protection legislation.

The main aims of the Consumer Duty are to set and test higher standards in respect of consumers and to reduce and prevent serious harm by:

- increasing trust placed in financial services by consumers;

- inspiring customer loyalty;

- levelling up standards across sectors; and

- boosting growth and driving competition.

1.2 Application – Who does the Consumer Duty apply to?

The Consumer Duty applies to all regulated firms that ‘determine or have a material influence’ over retail customer outcomes and not just those with a direct retail customer relationship. This will implicate firms involved in the manufacture, provision, sale and ongoing administration and management of financial products or services to end retail customers. See chapter 2 of FG22/5 for how the duty applies across the distribution chain.

Firms that have direct relationships with retail customers have the greatest responsibility and UK firms are expected to take reasonable steps to comply. FG22/5 notes this is an objective test. This means that the rules and guidance must be interpreted in line with the standard that could reasonably be expected of a prudent firm.

What is expected will include an assessment of the nature of the product or service being provided (eg, risk of harm to customers), the characteristics of the retail customer (eg, level of financial capability) and the firm’s role in relation to the product or service (including the firm’s role in the distribution chain).

Firms that outsource activities to third parties (eg, agents and distributors) will retain ultimate responsibility to meet the requirements and standards. Who is categorised as a retail client will depend on the regulated activity in question. The duty does not have a retrospective effect and does not apply to past actions by firms.

1.3 Consumer Duty components

The three key components to the Consumer Duty are set out below.

1.3.1 Principle 12

Consumer Duty introduced a new Principle for Business, Principle 12 which sets a higher-level expectation of conduct by the FCA and requires in-scope firms to ‘act to deliver good outcomes for retail customers’. See also chapter PRIN 2A: The Consumer Duty. This is the overall standard of conduct firms are expected to adhere to. Where Principle 12 applies, Principles 6 (treating customers fairly) and 7 (the requirement to be fair, clear and not misleading) do not apply. Where Principle 12 does not apply, Principles 6 and 7 will continue in effect.

1.3.2 Cross-cutting rules

Principle 12 is amplified by three cross-cutting rules which set out the overarching standards that firms must apply at all stages of the customer journey: on an individual level (eg, when providing customer support) and on a target-market level (eg, at the product design stage).

Firms must:

- act in good faith towards retail customers;

- avoid foreseeable harm to retail customers; and

- enable and support retail customers to pursue their financial objectives.

1.3.3 The four outcomes

The four outcomes, against which the FCA will measure firms, set out the rules, guidance and expectations for firm conduct in the firm-customer relationship are:

- The consumer understanding outcome – ensure that firms communicate, support and equip consumers to make informed decisions. Firms will need to ensure the information provided is what the customer needs, is made available at the right time, and is presented in a manner that is likely to be understood. This is particularly important for vulnerable customers.

- The price and value outcome – products and services should be sold at a price that reflects fair value where the amount paid is reasonably relative to the benefits of the product. There should be no excessively high fees and poor value products and services should be removed from markets.

- The product and service outcomes – the firm’s products and services should be fit for purpose, match the needs of customers and be appropriate for the target market. Firms will need to regularly monitor and review these areas.

- The consumer support outcome – customer needs should be supported throughout their relationship with the firm, including those customers considered to be vulnerable. Retail customers should not face unreasonable barriers (eg, when complaining, switching, or exiting a product).

See also section 3 which sets out some practical steps to compliance post-implementation.

1.4 Individual Conduct Rule 6

Individual Conduct Rule 6 was introduced as part of Consumer Duty – to ‘act to deliver good outcomes for retail customers’ where the firm’s activities fall within the scope of the Consumer Duty. This conduct rule applies to all staff. This means that:

- you must act in good faith towards retail customers;

- you must avoid causing foreseeable harm to retail customers; and

- you must enable and support retail customers to pursue their financial objectives.

In addition, senior managers must comply with Senior Manager Conduct Rules 2 and 3 to ensure they take all ‘reasonable steps’ to regulatory compliance. See Checklist: Embedding the Consumer Duty: practical considerations.

Section 2 – Delivering good customer outcomes

A key part of Consumer Duty compliance is that firms assess, test, understand and evidence the outcomes their customers are receiving. Without this information, it will not be possible for firms to know whether they are meeting the requirements. Integral to this is the data that firms are using to measure and monitor outcomes, and what ‘good’ looks like will vary depending on the nature of the firm, the product or service offered and the target market.

2.1 FCA monitoring and oversight

The FCA have frequently reminded firms that the Consumer Duty is not a ‘once and done’ exercise, and post-implementation, on a continual basis, firms should focus on whether they are delivering the outcomes for consumers that they set out to achieve. As part of their implementation planning, firms will have established frameworks to test, understand and evidence customer outcomes. Firms should regularly assess whether these processes are working and keep them under review, making improvements (as required).

2.2 FCA – Consumer Duty post-implementation reviews and focus areas

The FCA is actively engaging with firms sending out questionnaires to help gather information on how firms are implementing the Consumer Duty and delivering good outcomes for consumers. These questionnaires help the FCA to gather information and better understand approaches to embedding the Consumer Duty within firms. The FCA has issued a range of guidance on implementing the Duty in practice and publish findings of good and poor practice areas to highlight good practice and identify areas for improvement.

| Review/focus areas | Outcome | Published |

| Review of larger firms’ implementation of the Consumer Duty | Findings from review of firms’ plans to embed the Consumer Duty within their businesses. | 25 January 2023 |

| Review of fair value frameworks | Findings from review into firms’ approaches to fair value assessments under the Duty. | 10 May 2023 |

| Consumer Duty implementation: good and bad practice and areas for improvement | Builds on implementation and fair value framework review to remind firms of the consumer outcomes required by the Duty, sets out recent good practice and highlights areas for improvement. | 20 February 2024 |

| Price and Value Outcome: Good and Poor Practice update | Collates insights from the first year of implementation of the price and value outcome to help firms think about fair value assessments. | 18 September 2024 |

| Payments Consumer Duty multi-firm review | Key findings from review of payments firms’ implementation of the Consumer Duty. Whilst directed at payments firms, this review could be used as a reference guide by all in-scope firms. | 9 October 2024 |

| FCA Consumer Duty focus areas for 2024/5 | Webpage noting FCA priorities under the Consumer Duty for the remainder of 2024/5. The page provides a short description and expected timelines for ongoing and planned workstreams. Highlights four focus areas: embedding the Consumer Duty and raising standards, enhancing understanding of the price and value outcome, sector-specific priorities, and realising the benefits of the Consumer Duty. | 9 December 2024 |

| Consumer Duty Board Reports: good practice and areas for improvement | Presents findings of a targeted and thematic review of the first annual Consumer Duty board reports from 180 firms. It includes examples of good and poor practices to help firms enhance their board oversight and reporting processes. | 11 December 2024 |

| Complaints and root cause analysis: good practice and areas for improvement | FCA review into firms’ approaches to complaints and root cause analysis, based on a review of 40 firms across various sectors. While the FCA noted good processes for carrying out root cause analysis of complaints management information, they identified three key areas for improvement: analysing data for different customer types, taking action based on these insights, and assessing and measuring the impact of these actions. | 11 December 2024 |

| Review of firms’ treatment of customers in vulnerable circumstances | The FCA has confirmed that the existing guidance in FG21/1 remains a valuable and appropriate framework for firms. As such, there are no immediate plans to revise it. While the FCA found many positive examples of firms demonstrating a strong commitment to deliver good outcomes for customers, it also highlighted areas where improvements can be made. To support firms, the FCA published case studies providing evidence of good and poor practices to help signpost firms better support vulnerable customers. | 7 March 2025 |

| Delivering good outcomes for customers in vulnerable circumstances – good practice and areas for improvement | Results from the FCA’s multi-firm review in assessing how well firms are supporting customers in vulnerable circumstances under the Consumer Duty and FG21/1 guidance. Report provides examples of good and poor practice. Intended to help firms improve customer outcomes for vulnerable customers by renewing focus on customer identification, communications and continuous monitoring and oversight of outcomes to embed vulnerability considerations firm-wide. | 7 March 2025 |

| Consumer Support Outcome: good practices and areas for improvement | Findings from a thematic review of firms’ approaches to the ‘consumer support outcome’ highlights both good practices and areas requiring improvement. The report emphasises the importance of effective and proactive customer service to enable customers to realise the benefits of the products and services they buy and support them in pursuing their financial objectives. How firms implement the findings will depend on their business, size and circumstances. | 7 March 2025 |

| Consumer Duty review of requirements – feedback and next steps | The FCA has outlined a programme to simplify its regulatory framework in light of the Consumer Duty, aiming to streamline and modernise its approach to regulation. This will help to reduce complexity and enhance better outcomes for customers. | 25 March 2025 |

2.3 Dear CEO letters

By way of additional guidance, the FCA issued ‘Dear CEO’ portfolio and sector letters to provide specific feedback to firms on how they should embed the Consumer Duty. See Portfolio and sector letters. These reinforce the cross-sector findings of the implementation plan review and the FCA’s expectations – and set out examples of good and bad practices that may be helpful for firms to consider. Letters published after 31 July 2023 also contain information about post-implementation expectations and areas of focus.

On 25 March 2025, the FCA published a Feedback Statement (FS25/2), outlining its plan to simplify rules and guidance following the introduction of the Consumer Duty. The publication responds to feedback from the Call for Input issued in July 2024, which gathered 172 responses. FS25/2 details both immediate actions and longer-term plans, including accelerated consultations on high-priority areas and the withdrawal of outdated guidance and rules. The FCA also plans further industry engagement with a planned in-person summit scheduled for this summer and a comprehensive update on progress anticipated in September 2025.

Section 3 – Practical steps to post-implementation compliance

The FCA requires that firms demonstrate that they are acting to deliver good customer outcomes. Ways in which this can be done include those listed below.

3.1 Identification of data and assessment of outcomes – management information (MI)

Monitoring appropriate MI is key to identifying and managing any risks to good outcomes for customers. Firms will not know whether they are meeting the Consumer Duty requirements without appropriate MI. Firms should already hold MI to manage risks (eg, conduct risks and adherence to treating customers fairly), and this existing data can continue to be used and monitored. Recently, the FCA has said that firms should not just rely on the MI and data and think that is enough. They can use existing data and MI but they must regularly challenge themselves to see if it is adequate and provides them with enough information to assess whether they are delivering good outcomes. See section 2 on culture, governance and monitoring in the FCA’s ‘Consumer Duty implementation: good practice and areas for improvement’.

The FCA has not prescribed what sources of data firms should use to assess whether they are delivering good outcomes, and each firm should decide based on several factors including its size, client base and nature of the business (see chapter 11 of the finalised guidance for examples of the types of data firms could collect). Firms working with third-party agents or distributors should share feedback on a regular basis and have established regular monitoring and oversight of sales processes to enable them to monitor whether the outsourced service is supporting good consumer outcomes.

Monitoring will be more frequent in some cases (eg, customer support, transactions, complaints), and this should be reviewed on an ongoing basis. There may be a requirement to produce MI where issues have been identified with a product or a particular adviser. MI should be scrutinised and challenged and must enable firms to identify where customers are experiencing problems. Firms should also be considering whether the MI they have is giving them the information they need and if it is not, they should be obtaining the information they need (this may require system changes or introducing ways of capturing information).

Firms must take appropriate action to remedy the situation and keep records of their approach and outcomes. Develop a clear plan to gather the right information and ensure it is being used effectively to demonstrate good customer outcomes. The FCA is actively challenging the MI provided by boards – it is not enough to provide vague, unsupported generic statements such as ‘we believe our products are performing as intended’. It is likely the processes to capture data and MI will evolve over time, (eg, with increasing automation to streamline processes).

Outsourced or third-party providers need arrangements to capture data necessary to monitor whether they deliver good outcomes on the firm’s behalf. It is necessary to understand the underlying reasons behind data collection, why it is being collected and what firms are going to do with it. Firms working with non-UK firms in their distribution chain will also need to consider how they will ‘train’ non-UK firms on the MI required to evidence compliance.

Some examples of the types of data and information that firms could use are set out below.

3.2 Meeting the needs of vulnerable customers

Taking practical action to respond to the needs of vulnerable customers is a key priority for the FCA and a key feature of the new Consumer Duty requirement. The Consumer Duty emphasises the importance of suitability and appropriateness of products and services to the target market and delivering good consumer outcomes. The FCA urges firms to consider this new rule and guidance alongside existing guidance on the fair treatment of vulnerable customers (FG21/1). On 15 March 2024, the FCA announced a review into how firms are acting to understand and respond to the needs of vulnerable customers. The findings, published on 7 March 2025, assess whether firms are meeting the expectations set out in FG21/1 and highlight areas of good and poor practice across sectors. The review also considers that the existing guidance in FG21/1 remains relevant and useful under the Consumer Duty framework and the FCA has published case studies to assist firms with compliance.

A vulnerable customer is ‘someone who, due to their personal circumstances, is especially susceptible to detriment, particularly when a firm is not acting with appropriate levels of care’. The definition is very broad and the FCA expects firms to pay attention to the needs of customers with characteristics of vulnerability at all stages of the customer journey.

Vulnerability can be difficult to identify as it may take many different forms, and it may not always be obvious – it may be hidden, permanent or temporary and not all customers can be managed in the same way. Vulnerability is not limited to personal characteristics, and may relate to personal circumstances (eg, a change in relationship status, an unwell relative or a recent redundancy). The FCA has highlighted that firms should ensure that products do not have features which exploit customers, such as charging unjustifiably or unreasonably high fees or interest rates to groups including those with characteristics of vulnerability. Practically speaking, this is applicable across many areas of product sales, design and development, and a checklist of considerations for firms is set out below:

3.3 Steps to fulfil price and value outcome – fair value assessments

The FCA has highlighted the importance of conducting fair value assessments to fulfil the price and value outcome of the Consumer Duty. As noted above, the Price and Value Outcome: Good and Poor Practice update was published in October 2024.

Some of the FCA findings are as follows:

- some firms use complex pricing structures that customers might not understand;

- firms grouping materially different products together when completing fair value assessments can affect the accuracy of the assessment;

- firms define their target markets too broadly meaning that some customers may not get good value from the products;

- firms stating that products provide fair value without providing supporting analysis or evidence;

- firms comparing products to a more favourable part of the market when benchmarking products against the competition can make their products seem better than they are;

- firms not having adequate processes in place to identify and support vulnerable customers;

- firms providing insufficient information to explain how the cost of a product relates to fair value; and

- firms not being able to provide evidence of how material issues in fair value assessments are reported to the Board.

3.3.1 What is fair value?

Fair value is about more than price. Value should include consideration of the quality, limitations and benefits of the product or service. Firms should consider what fair value means in the context of their business models, products, and services to customers, and ensure that the price the customer pays for a product or service is reasonable when compared with the overall benefits. In essence, firms should undertake a cost–benefit analysis. Value needs to be considered in the round and the FCA has been very clear that low prices do not always mean fair value.

3.3.2 Practical considerations

Aspects aside from price and value which firms should consider include:

- Whether they are meeting the other three Consumer Duty outcomes (see above at section 1.3.3) as they will have to take a holistic view in working out whether products and services provide value fairly.

- Who their target market is, as this will help firms to understand their customer needs and develop the level of service and communications they will require. For existing or new products and services firms should look at the cost of designing a product or service and the projected revenue (eg, with new products this could include the costs of IT charges, marketing campaigns, preparation of communications and staff recruitment).

- Fees charged by their competitors for a similar product, whether the firm is an outlier and there is a reasonable justification for this, such as the firm’s customers are provided with a higher level of personal service than the competition.

- Are there any limitations attaching to a product or service which impacts the value received by the customer. For example, there are lengthy notice periods applicable if customers want to switch to another product or provider.

In the fair value framework review, the FCA acknowledged the challenges involved in meeting the fair price and value outcome including that:

- many of the fair value assessments do not rely on solid data and other credible evidence to justify the products’ value to retail customers; and

- the ‘length’ of the value in the distribution chain, as there may be fees added along the way (eg, fees for ongoing management, penalty or transaction fees).

When making the fair value assessment, firms should be aware that a product or service that does not meet the needs of customers or offer them any benefit is unlikely to offer fair value whatever the price.

Firms should look at both the benefits and limitations of the products and services including the performance, quality of service and communications as well as benchmarking across other products or services (this can be done across the internal product or services offered, or across those of competitors).

Firms must consider price in the context of the following:

- Customer groups – are regular and occasional customers being charged the same fee? This is relevant in the wealth space – consider where customers who have sporadic engagement with a firm are paying the same monthly fees as customers who engage on a regular basis – is this fair?

- Differences between fees paid by recent onboards or customers where discounts have been applied or long-standing customers who may be in higher fee tariffs.

- Whether any disadvantage in rates levied to vulnerable customers (eg, customers who have defaulted in the past may be on higher rates) – is this fair or is this making a bad situation worse?

- Consider the cost of developing and providing the product and compare that to how much revenue you are making from it – is the differential fair?

- There needs to be robust governance – the board and senior management should be fully engaged and challenged where necessary.

3.4 Consumer Duty – impact on culture and governance

There is a direct link between culture and compliance, and the FCA expects the focus on acting to deliver good outcomes to be at the heart of firms’ strategies and business objectives.

Firms are required to:

- report evidence of good outcomes to their board and report this for sign-off at least annually. This should be effectively scrutinised and proactive plans should be in place to address any gaps. Board reports will come under scrutiny as the FCA will be seeking evidence of the steps firms are taking to drive good outcomes. The FCA may ask to see the board report along with supporting data and these should be sufficiently robust to demonstrate not only compliance but address areas of non-compliance or where improvement is needed. Ensure that board reports evidence challenge from senior managers and board minutes provide evidence of this level of scrutiny;

- ensure that the Duty is embedded in firm culture, governance, leadership and incentive structures, with outcomes for retail customers central to risk and audit processes. While firms were previously expected to appoint a Consumer Duty champion, this is no longer required from 27 February 2025. However, firms may retain the role if they find it helpful for maintaining focus on consumer outcomes;

- provide training for staff to ensure they understand their role in delivering good outcomes; and

- remain proactive and alert to FCA guidance and consider how it applies;

- regularly review and monitor outcomes as part of ongoing compliance, including maintaining and enhancing board reporting processes; and

- consider the range of metrics and feedback mechanisms for testing whether the level of support leads to good outcomes. In the words of the FCA, ‘the Duty isn’t something you can tick the Consumer Duty box on your to-do list and move on’. See Consumer Duty: Not once and done.

3.5 Consumer Duty – FCA supervision and enforcement

The Consumer Duty remains a top priority for the FCA, and they are committed to taking robust action. Their approach to supervision and enforcement will be proportionate to the harm or risk of harm to consumers. They will act ‘swiftly and assertively’ where they find evidence of harm, with the most serious breaches being prioritised. In his speech on 20 February 2024, Sheldon Mills, Executive Director, Consumers and Competition, FCA noted that ‘at all times, when supervising and enforcing the Duty, we will be informed by data and metrics as to where we prioritise our focus’. In some cases, firms can expect sanctions such as interventions or investigations along with possible disciplinary action.

Additional resources

FCA

Consumer Duty webpage (provides links to final rules, guidance and useful resources)

Related Lexology Pro content

Checklist:

Embedding the Consumer Duty: practical considerations

Reliance on information posted:

While we use reasonable endeavours to provide up to date and relevant materials, the materials posted on our site are not intended to amount to advice on which reliance should be placed. They may not reflect recent changes in the law and are not intended to constitute a definitive or complete statement of the law. You may use them to stay up to date with legal developments but you should not use them for transactions or legal advice and you should carry out your own research. We therefore disclaim all liability and responsibility arising from any reliance placed on such materials by any visitor to our site, or by anyone who may be informed of any of its contents.