Background

On 28 November 2024, the Treasury Laws Amendment (Mergers and Acquisitions Reform) Act 2024 (hereinafter referred to as ‘the Act’) was passed by Parliament. This represents the most substantial change to merger laws in more than 50 years, moving from a voluntary, informal review process to a mandatory and suspensory notification regime.

On 27 March 2025, the Australian Competition and Consumer Commission (ACCC) released draft guidance on how it will assess acquisitions under the new merger regime.

Read our previous overview of the ACCC’s proposed guidance and our advice on how to prepare for these key changes.

Introduction

From 1 January 2026, parties will be required to notify the ACCC regarding acquisitions that meet prescribed thresholds and must not complete those transactions without prior ACCC approval. The regime applies to acquisitions of assets, shares, units in a unit trust, and interests in a managed investment scheme.

In June 2025, the Federal Government made the Competition and Consumer (Notification of Acquisitions) Determination 2025, which sets out the prescribed thresholds and introduces additional notification requirements for major supermarkets.

A transitional voluntary regime has been in effect since 1 July 2025. This remains in place until 31 December 2025, after which it will be replaced by a mandatory notification and clearance process outlined below.

As a recent development, the government announced on 1 December 2025 that the new asset thresholds and control thresholds will commence on 1 April 2026. This delay is to give businesses time to prepare for these aspects. However, the core merger control regime will commence as planned on 1 January 2026. The final provisions are expected to be registered on the Federal Register of Legislation in mid-December 2025.

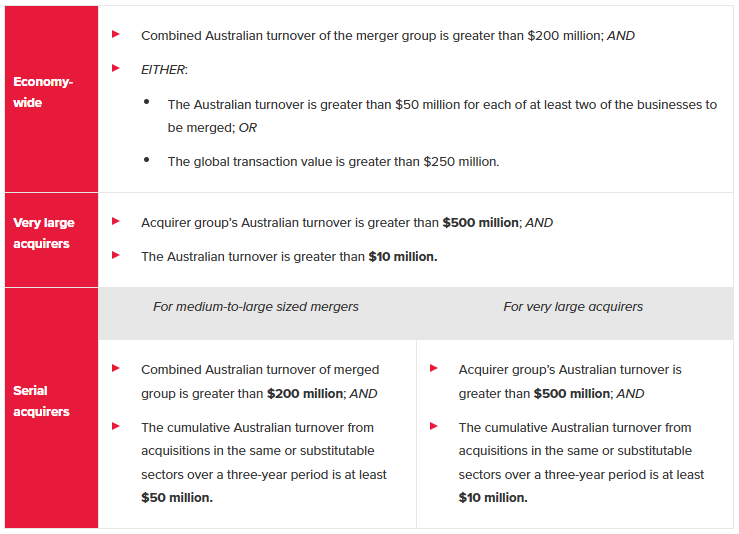

Monetary thresholds

The ACCC has set out thresholds for three general circumstances in which a notification must be made. All figures in AUD.

Note: Where the acquisition is a ‘small acquisition’, these will be excluded from the new regime.

Key definitions:

Australian turnover: An entity’s Australian turnover is the amount of the entity’s gross revenue, determined in accordance with Accounting Standards, for its most recent twelve-month financial reporting period, attributable to transactions or assets within Australia, or transactions into Australia.

Connected entities: A 'connected entity' is a 'related entity' as referred to in section 4A of the Act (subsidiary, holding and related bodies corporate), or an entity that is controlled by, controls, or is under common control with the first entity, for the purposes of section 50AA of the Corporations Act 2001 (Cth).

Small acquisition: Where the Australian turnover of the target (and its connected entities) is less than $2 million.

Connection to Australia

In order to be notifiable, an acquisition must first be 'connected to Australia', meaning that:

- In relation to the acquisition of shares or other interests in a body corporate, the body corporate carries on a business in Australia or;

- In relation to the acquisition of assets, the assets are used in, or form part of, a business carried on in Australia.

Three-year look back test for serial acquirers

The three-year cumulative test set out in the table above for serial acquirers means that once an acquirer group meets the cumulative threshold test in a given three-year period, every additional transaction over $2 million that the acquirer makes in the same or substitutable sector will need to be notified to the ACCC during that three-year period.

Further, when the ACCC is considering a proposed transaction, it will have the ability to aggregate the effect of that particular transaction with the effect of all other acquisitions by the acquirer where the target was involved in the supply of the same or substitutable goods or services (disregarding any geographical factors or limitations) in the previous three years.

This will have significant implications for parties in the process of, or proposing to, roll up several smaller targets in an industry as part of an inorganic growth strategy, including private equity funds.

Exceptions to the notifications thresholds

There are some exceptions to the notifications thresholds:

- Acquisitions which do not result in control of the target business, or which result in less than 20 per cent of the voting power in a publicly listed entity are exempt

- Regardless of the above thresholds, major supermarkets (at this stage Woolworths and Coles) must notify acquisitions of a supermarket business or land for a supermarket business. There are currently no other sector-specific classes of transactions

- Further exemptions apply for certain types of transactions. These include, but are not limited to:

- Transactions by liquidators, administrators and receivers in insolvency matters

- Transfers arising due to inheritance, intestacy or joint tenancy survivorship

- Land acquired for certain purposes

- Shares resulting from capital raisings, rights issues and buy-backs

- Security interests over shares or assets in relation to financial accommodation on ordinary commercial terms.

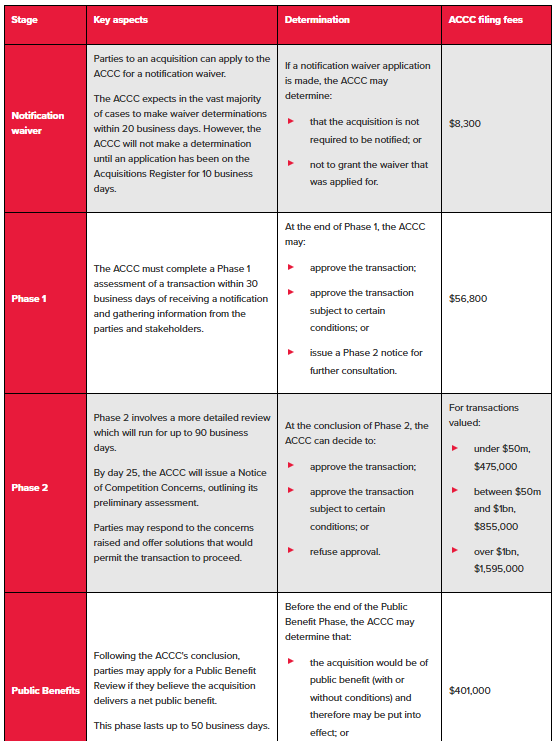

ACCC review and determination process

The ACCC has indicated that it expects most transactions will be approved within Phase 1 and a limited number of transactions will proceed to the Public Benefits phase.

Filling fees are cumulative. For example, an acquisition that proceeds from Phase 1 to Phase 2 to a Public Benefits assessment will have to pay the prescribed fee at each stage of the assessment. There are no additional fees for timeline extensions.

Failure to notify

If the parties choose not to notify an acquisition that is required to be notified, the acquisition is stayed – that is, it cannot be put into effect.

If an acquisition is put into effect while stayed, this is a contravention of the Act and the acquisition will be void. Significant penalties may also be imposed by the court.

The maximum penalty for a contravention by a corporation is the greater of:

- $50 million;

- three times the value of the reasonable attributable benefit obtained (if that can be determined), or;

- where the benefit cannot be determined, 30 per cent of the corporation’s adjusted turnover during the breach turnover period for the contravention.

If there is doubt about whether an acquisition needs to be notified, parties to an acquisition may request a notification waiver in certain circumstances or notify the ACCC voluntarily.

The ACCC will be taking an active monitoring and surveillance role to ensure compliance with the mandatory requirements.

Key takeaways

The new merger regime is expected to have a significant impact on Australian M&A transactions, including:

- Increased scrutiny: More thorough reviews of proposed M&A activity, resulting in longer timelines for deal approvals.

- Higher transaction costs: Organisations will need to invest more in legal and compliance resources to navigate the new regulatory landscape, including preparing detailed submissions to the ACCC, in addition to the ACCC filing fees outlined above.

- Strategic planning: Strategic planning on transactions will be a priority, considering the new thresholds and the potential for increased regulatory intervention.

- Market uncertainty: There will be greater uncertainty at the start of 2026 as organisations and regulators adjust to the new regime.

- Undertaking comprehensive due diligence: Ensuring proposed transactions do not raise red flags and are supported by strong competition analysis and collect all information required by the ACCC during due diligence.

- Increased transparency: The ACCC will offer insight into their thinking by publishing reasons for all final decisions.

- Early engagement with the ACCC: Via the pre-notification process to understand requirements and avoid delays.

- Increased prevalence of Material Adverse Change (MAC) clauses: As regulatory scrutiny increases under the new merger regime, MAC clauses are expected to become more prevalent in transaction agreements. These clauses allow parties to terminate a deal if a significant negative event occurs that materially affects the company between signing and completion. A recent Federal Court decision in Cosette Pharmaceuticals Inc v Mayne Pharma Group Limited (15 October 2025) has provided important guidance on the enforceability of MAC clauses in Australian M&A transactions, including clarifying how courts interpret materiality and timing, reinforcing the importance of clear drafting and risk allocation in deal documentation.