When ASIC released its Capital Markets Roadmap (REP 823) in November, it foreshadowed the introduction of an “easily-referenced regulatory guidance catalogue” for funds management. That commitment has now materialised: ASIC’s Regulatory Catalogue for Private Credit and Funds Management consolidates, in a single resource, the core legislative provisions, regulatory guides, information sheets and class orders that apply across the life-cycle of a fund.

For Australia’s rapidly expanding A$200 billion private credit sector, encompassing both wholesale and retail offerings, the Catalogue is more than a reference tool. It provides a clear, practical framework for compliance, sets out ASIC’s expectations, and signals a shift towards more data-driven surveillance and enforcement. Importantly, it extends ASIC’s supervisory focus beyond retail funds, bringing greater transparency and accountability to wholesale markets that have historically operated with less regulatory scrutiny, and related market participants such as Registered Entities.

Key messages at a glance

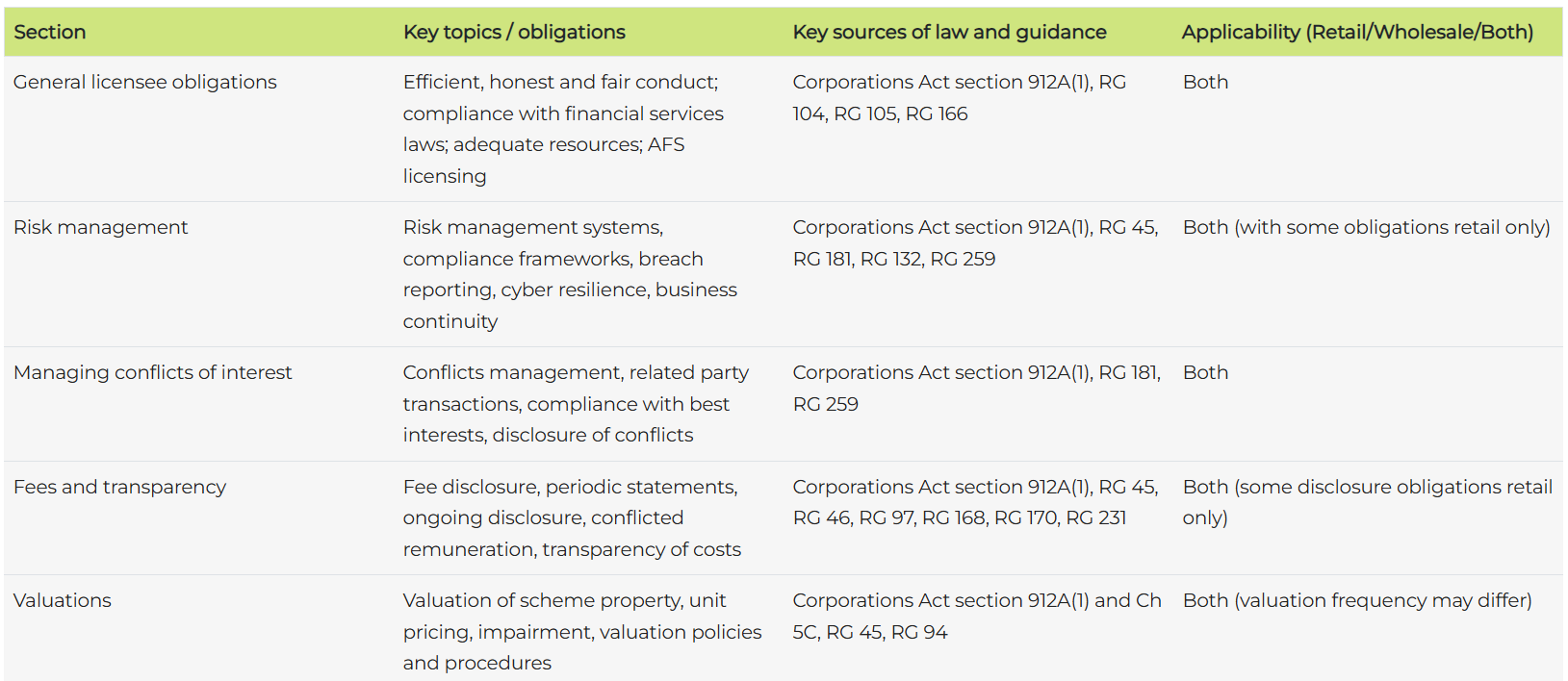

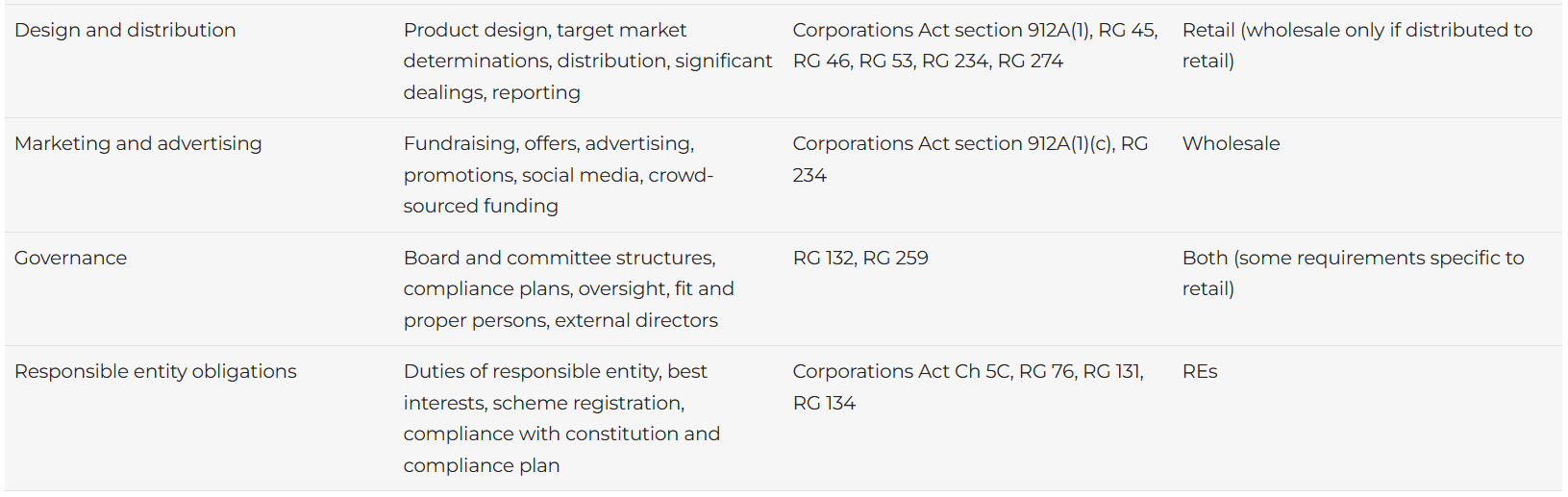

The Catalogue brings together more than 70 primary legal obligations and over 40 pieces of ASIC guidance into a single, interactive index, structured around nine thematic pillars. While many requirements will be familiar, the consolidated format highlights compliance gaps, particularly for wholesale managers who have historically relied on exemptions or legacy interpretations.

ASIC has positioned the Catalogue as the foundation for its 2026-27 guidance refresh and for more targeted, data-driven surveillance. Market participants should expect future data requests and reviews to be mapped directly to Catalogue line items. Fund managers, responsible entities (REs), trustees, platform operators and advisers should treat the Catalogue as essential reading and use it as a checklist for immediate compliance gap analysis.

How the Catalogue is organised

ASIC has adopted a “life-cycle plus overlay” model:

What is new – and why it matters

While the Catalogue does not introduce new law, several features are particularly noteworthy.

First, application to both retail and wholesale funds. The Catalogue addresses obligations relevant to both retail and wholesale fund operators, and highlights where certain requirements apply to each. Notably, the Catalogue brings together obligations that may have previously been considered as primarily relevant to retail funds, such as misleading or deceptive conduct, and valuation practices, and clarifies their relevance for wholesale fund operators as well.

Alignment with REP 820’s ten principles. The Catalogue references the private credit “better practice” principles (governance, conflicts, valuations, liquidity, credit risk, etc.) articulated in REP 820, and encourages industry to benchmark their practices against these principles. However, the Catalogue does not systematically cross-reference each obligation to these principles.

Implications for legal compliance and risk management

-

No room for ambiguity. The Catalogue’s clarity means ASIC will expect operators to proactively remediate gaps and promptly remediate compliance gaps. Claims of ignorance or complexity are unlikely to be persuasive in future regulatory interactions.

-

Increased governance expectations. The Catalogue highlights ASIC’s expectation that boards, not just compliance teams, are ultimately responsible for adherence to regulatory obligations. For superannuation trustees and platform operators already under APRA scrutiny, misalignment with the Catalogue increases prudential and regulatory risk.

-

Valuation and liquidity under the microscope. The high-priority pillars directly address systemic risk. Funds without robust, independently-reviewed valuations, clear impairment policies, or stress-tested liquidity frameworks should anticipate heightened regulatory attention.

-

Diminishing wholesale carve-outs. The Catalogue’s consolidation of obligations for both retail and wholesale funds signals ASIC’s intent to pursue legislative reform that will bring registered and unregistered schemes into closer alignment, including requirements for wholesale scheme notification, audited accounts, and statutory duties.

-

Elevated distribution due diligence. Platform and RE due diligence teams should now incorporate adherence of the items set out in the Catalogue into product onboarding and ongoing monitoring.

Potential challenges for market participants

Resource constraints. Smaller managers may lack the compliance resources to map, monitor, and evidence adherence to the Catalogue’s extensive obligations.

Systems capability. Generating granular data (such as loan-level, fee capture, and related-party metrics) on demand may challenge legacy administration systems.

Managing intra-group conflicts. The Catalogue brings renewed scrutiny to vertical integration and conflicts of interest, which may impact the business models of various market participants.

Board and director education. Non-executive directors must demonstrably engage with a broader compliance brief; ASIC have clearly articulated compliance obligations and will expect action.

Audit and assurance alignment. External auditors are likely to align their testing programs to the Catalogue, increasing expectations for documentation and evidence.

Practical steps – our recommended response plan

-

Immediate triage: Download the Catalogue and assign internal responsibility. Conduct a gap analysis, mapping existing policies, registers, and monitoring tools against Catalogue requirements. Identify and implement quick wins (such as updating disclosure templates) and address structural gaps (such as independent valuation mandates).

-

Board-level attestation: Present the gap analysis to the board or investment committee and secure board commitment to regular (ideally annual) Catalogue compliance attestations.

-

Enhance reporting architecture: Assess whether current systems can generate, on short notice, the data points highlighted in the ASIC's market messaging to date (e.g., borrower-level pricing, impairment review frequency, redemption queue metrics). Introduce plans to address gaps.

-

Refresh conflicts and remuneration frameworks: Review arrangements for commissions and fees. Benchmark frameworks against the latest RG 181 updates and REP 820 better-practice examples.

-

Strengthen valuation and liquidity protocols: Move towards regular, independently-reviewed valuations for all material positions. Document trigger-based impairment and distribution coverage metrics. Stress-test liquidity (including redemption, financing, and market risk) and ensure outcomes are reflected in PDS/TMD disclosures.

-

Training and culture: Provide targeted compliance training for directors, investment teams, distribution staff, and outsourced service providers. Update audit and risk committee charters to include obligations oversight.

-

Engage with ASIC early: Where legacy structures or commercial constraints make immediate compliance challenging, develop a credible transition plan and engage proactively with ASIC.

Looking ahead

The Catalogue is not the final destination; it provides the foundation for ASIC’s 2026–27 regulatory guidance refresh and a new era of intensified surveillance. Private credit participants who use the Catalogue to embed robust compliance practices, rather than treating it as a static checklist, will be best positioned to navigate the next phase of market reform.