Tax Guide for Foreign Artists Performing in the United States

Many performing artists dream of performing in the United States. The sheer size of the U.S. market represents tremendous financial opportunity for musicians, actors, athletes, and other pro-level performers.

But without some prior planning, the U.S. tax code can make it difficult to run a profitable tour.

Specifically, the U.S. imposes a special 30 percent withholding of touring, performance, and even merchandising revenues associated with U.S. performances.

It’s very difficult to avoid this withholding: Concert and performance venues are required to deduct 30 percent of artist revenues before you even see it, and forward it to the IRS.

You can apply for a partial refund later by documenting business and touring expenses. But in the meantime, that withholding requirement can present a major cash flow problem for performing artists: You still need to pay full price for travel, lodging, crew labor, insurance, and other expenses.

Some countries have negotiated tax treaties with the United States, arranging more favorable tax treatment for their artists. But most non-U.S. artists are still subject to the withholding requirement, unless other arrangements are negotiated with the IRS in advance.

This article is for non-U.S. performing artists and athletes and their management teams who want to maximize the after-tax cash flow and profitability of U.S. tours and performance engagements. We’ll discuss the importance of cash flow to U.S. tours and how to negotiate a central withholding agreement with the IRS to reduce the 30% withholding requirement and preserve cash flow.

We’ll also discuss countries that have favorable treaty arrangements with the U.S., and how artists from these countries can claim treaty benefits.

Background – The 30% Withholding Problem

The general rule is this: The IRS knows that it is extremely difficult to collect taxes owed from foreign performing artists who leave the U.S.

In October 2007, the IRS launched a dedicated task force focused on “improving U.S. income reporting and tax payment compliance by foreign artists who work in the United States.”

And so in early 2011, the IRS began stepping up enforcement by directing performance venues to withhold 30% of gross compensation from foreign artists, and forward it to the IRS against expected tax liability.

For example, if the performance fee or artist’s share ticket proceeds were $10,000, the IRS required the venue to subtract $3,000 from gross revenues and forward it to the IRS. Artists would receive $7,000, and a letter explaining the withholding.

Often, artists received little warning and had no opportunity for appeal.

To make matters worse, unless the artist or their management made other arrangements in advance, the 30% withholding would come out of the gross receipts–not the net–at each venue. Meanwhile, artists or their managers/labels must cover all the touring travel, lodging, labor, insurance, promotion, and equipment costs out of what was left over after the withholding.

For artists with significant tour expenses, this often means paying far more in withholding than their actual tax liability on net income.

Example: A UK-based rock band went on a tour of the United States. Between ticket sales and merchandising, they generated gross earnings of $100,000, with $60,000 in legitimate touring and promotional expenses. Total profits therefore amounted to $40,000.

If they were U.S. residents, their income tax liability on that $40,000 net income would be roughly $6,000-$8,000.

But because these musicians were non-resident aliens under U.S. law, the 30% default withholding requirement applied: Out of their $100,000 in gross receipts, the venues subtracted $30,000 from their fees and other revenues up front—five times their actual tax bill.

This creates immediate cash flow problems that can make it extremely difficult to put together a successful tour.

What Income Gets Taxed

The IRS treats foreign artist income differently than U.S. resident personal and business income.

If you’re a non-resident alien performing in the U.S., you can expect withholding to apply to all of the following types of revenue:

- Performance fees, appearance fees, headliner bonuses

- Meet-and-greet experiences, VIP packages, fan club events

- “Merch” sales at venues and even online sales during tour periods (if payments are controlled by U.S. venues)

- Endorsement deals and brand partnerships tied to U.S. performances

- Streaming revenue from shows recorded in the U.S.

Even money venues pay to management companies rather than directly to the artist can be “looked through” and taxed as personal income under anti-avoidance rules.

That means, payments routed through loan-out/management entities often do not avoid U.S. withholding; withholding agents may still have to withhold unless a valid CWA is in place, or a tax treaty exists establishing lower withholding.

Additional State Withholding on Non-U.S. Artist Revenues

Certain high-tax states like California and New York add additional withholding requirements on their venues, on top of the 30% base withholding. For example, California adds another 7% withholding on payments over $1,500 to nonresidents.

However, you can reduce that withholding requirement by filing Forms 587-590 showing that your allocation of revenues to California is lower than your overall gross payments.

Example: A band earning $50,000 on a 10-city tour with 2 California shows might allocate just $10,000 to California, reducing withholding from $3,500 to $700. Source: California FTB Forms

Other State Withholding Requirements

- Massachusetts imposes a 5% withholding requirement on amounts exceeding $5,000.

- Minnesota has a 2% withholding requirement on amounts over $600.

- Missouri has a 2% withholding requirement on payments exceeding $300

- North Carolina has a 4% withholding requirement on amounts over $1,500

- Wisconsin has a 6% withholding requirement on amounts over $7,000.

- New York sources compensation to in-state performances and related services. Slightly different rules apply to athletes competing in New York.

Combined, state and federal withholding can amount to nearly 40% of your total revenue before paying tour expenses. So reducing overall withholding can make a big difference when it comes to financing a U.S. tour.

Improve Your Cash Flow: Negotiate a Central Withholding Agreement With the IRS

Fortunately, it doesn’t have to be that way. Instead, non-U.S. artists or their management teams can negotiate a central withholding agreement (CWA) with the IRS.

Under this framework, artists submit projections of their touring and other business expenses to the IRS in advance. The IRS then agrees to reduce their withholding requirement to more realistic levels.

By negotiating a CWA with the IRS, artists can potentially reduce required withholding from 30% of gross income to as little as 10-15% of net income.

This frees up substantial cash flow you can use to finance tour expenses.

To accomplish negotiating a central withholding agreement (CWA) in advance that reduces withholding to more reasonable and realistic levels.

Proper planning can potentially save artists many thousands of dollars for a tour or series of engagements.

It can mean the difference between a profitable or unprofitable tour.

A central withholding agreement is a contract between a foreign (non-U.S.) performing artist and the IRS that sets up a customized tax withholding arrangement for their U.S.-sourced income.

Instead of submitting to the full 30% withholding on all gross revenues that normally applies, the IRS agrees in advance to withhold tax only on the artist’s estimated net income after expenses.

CWA Planning Timelines

Successfully negotiating a CWA requires advance planning. Here’s a rough timeline you can use for your planning purposes

- 90+ days before first performance or deposit: Begin CWA planning and gather documentation.

- 45+ days before the first show: Submit your complete CWA application. This is a hard deadline and cannot be waived.

- During your tour: Maintain detailed expense records and day-by-day logs for state tax purposes.

- After your tour: File required returns (Form 1040-NR) to submit refund claims for any overpayments.

How To Claim Tax Treaty Benefits

Some countries have negotiated a more advantageous withholding arrangement with the U.S. Treaty provisions for artists vary widely; many still let the U.S. tax non-U.S. performers (Article 17), but using more favorable revenue thresholds.

Not every country has a tax treaty with the U.S. And specific provisions vary widely from country to country.

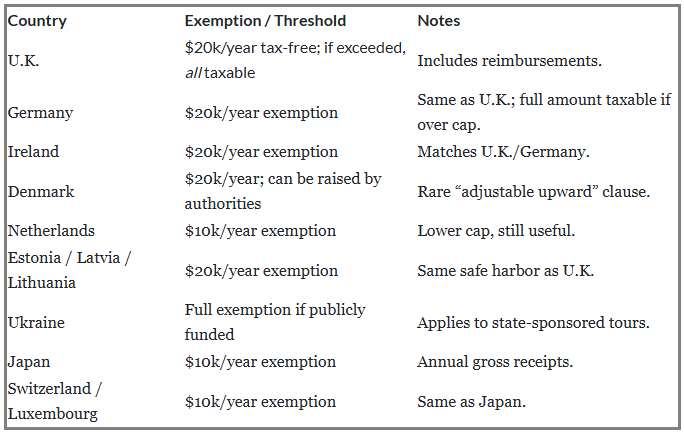

For example, The U.S.–U.K. Income Tax Treaty generally permits U.K. resident artists to earn up to $20,000 tax-free (for personal services performed in the U.S.) during a tax year. However, once this threshold is exceeded, the entire income becomes subject to U.S. taxation—not just the amount over $20,000.

Note that this incentivizes shorter U.S. tours and one-off performances for U.K.-based performance artists).

Here is a brief table of some of the more favorable U.S. tax treaties with regard to performing artists:

Favorable U.S. Tax Treaties for Performers

If your country has a tax treaty with the United States, you can view the treaty here.