Starting 1 January 2025, many large Australian businesses and financial institutions must now prepare annual sustainability reports containing mandatory climate-related financial disclosures, with the Australian Securities and Investments Commission (ASIC) last week releasing its final guidance on sustainability reporting to assist entities to comply with their sustainability reporting obligations. This is consistent with global momentum on mandatory climate reporting, with the International Financial Reporting Standards (IFRS) Foundation’s recent progress report finding 30 jurisdictions have decided to use or are taking steps to introduce the international sustainability standards in their legal or regulatory frameworks, as of September 2024.

However, there are some notable jurisdictions moving to delay or pare back their mandatory climate reporting regimes. This alert considers the latest regulatory changes and delays which we have observed in key jurisdictions overseas, and the implications for Australian companies.

Regulatory changes and delays observed overseas

European Union (EU)

As part of its EU Green Deal package of policy initiatives designed to set the EU on a path to achieving climate neutrality by 2050, the Commission had previously introduced the following directives and regulations:

- the Corporate Sustainability Reporting Directive (CSRD), to strengthen and broaden the EU’s existing regulatory framework, the Non-Financial Reporting Directive, and establish binding sustainability reporting standards, among other things;

- the EU Taxonomy for sustainable activities, to establish a classification system to clarify which economic activities are environmentally sustainable to direct investments to the economic activities most needed for the transition, in line with Green Deal objectives;

- the Corporate Sustainability Due Diligence Directive (CSDDD), to foster sustainable and responsible corporate behaviour in companies’ operations and global value chains by ensuring that companies in scope identify and address adverse human rights and environmental impacts of their actions within Europe and beyond; and

- the Carbon Border Adjustment Mechanism (CBAM), to effectively impose a carbon tariff on all goods and parts imported into the EU to encourage cleaner industrial production in non-EU countries. CBAM aims to ensure that the carbon price of imports is equivalent to the carbon price of domestic production.

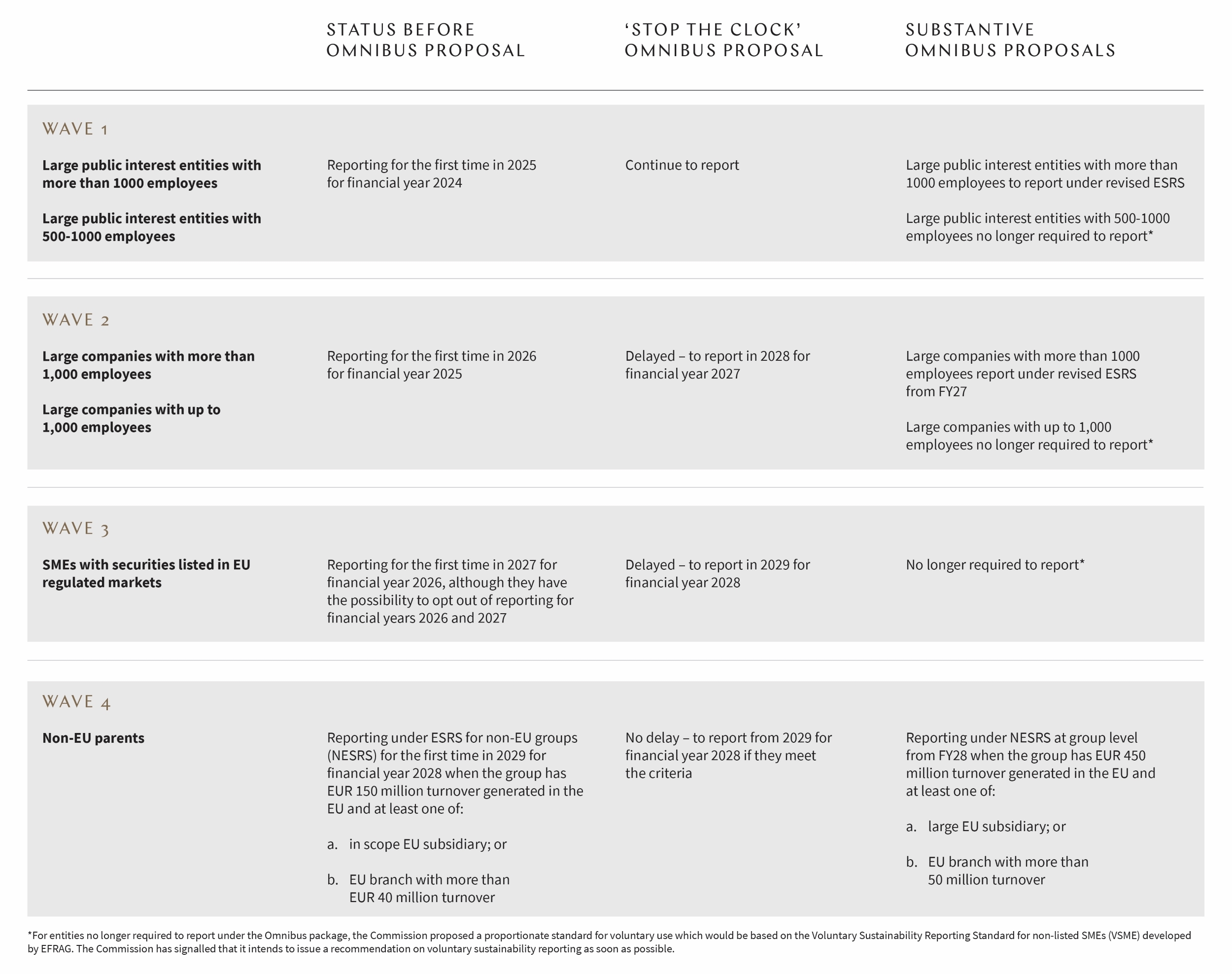

However, on 26 February 2025, the EU Commission (Commission) adopted an Omnibus package of proposals to simplify the CSRD, the CSDDD, the EU Taxonomy, CBAM and other Green Deal regulations.

In adopting the Omnibus package of simplification proposals, the Commission sought to recalibrate to foster a favourable business environment to ensure that companies are not stifled by excessive regulatory burdens.

Among other things, under this Omnibus package:

- only the largest companies would report under the European Sustainability Reporting Standards (ESRS) and a subset of those companies would continue to report under the EU Taxonomy;

- the EU Taxonomy would now only apply for a subset of large companies being those with more than 1000 employees or a net turnover of more than EUR 450 million;

- the Commission also no longer plans to adopt sector-specific standards and has tasked the European Financial Reporting Advisory Group (EFRAG) with amending the ESRS to substantially reduce the volume of disclosures – these draft amendments are due to the Commission by 31 October 2025; and

- postpones the start dates for the CSRD by two years and by one year for the CSDDD as part of a “stop the clock” proposal to reduce the regulatory burden on certain companies and provide them with additional time to prepare for compliance amidst ongoing debates about broader simplifications to the EU’s sustainability framework (discussed further below).

By seeking to create a more favourable business environment, the EU hopes to enable companies to embrace the transition into a sustainable economy in a more effective and pragmatic way by making the rules fit for purpose, more proportionate and more appealing.

In March 2025, the EU Council announced that they had approved the Commission’s “stop the clock” directive. The EU Parliament adopted this directive on 3 April 2025. The directive will enter into force following formal approval by the EU Council, with member states required to transpose it into national law by 31 December 2025.

An overview of the Omnibus proposals is below:

In the meantime, however, there is continued progress in other areas including recent announcements that the EU’s Platform on Sustainable Finance (PSF), an expert group mandated by the Commission to advise it on the development of sustainable finance policies, was proposing a new “SME sustainable finance standard” aimed at helping small and medium-sized enterprises to access external financing to support their sustainability and climate transition-related initiatives.

The Sustainable Finance Disclosure Regulation also remains on foot for EU-based fund managers and other financial market participants, requiring them to disclose how they incorporate sustainability risks and opportunities into their investment strategies and products. However, the Commission is currently carrying out a comprehensive assessment of the framework, looking at issues such as legal certainty, usability and how the framework can play its part in tackling greenwashing.

United States of America

In March 2025, the US Securities and Exchange Commission (SEC) decided to withdraw its legal defence of its climate disclosure rules, signalling a shift in approach under the Trump administration.

The SEC’s climate disclosure rules for public companies and in public offerings were originally adopted in 2024 and had been suspended due to a number of legal challenges. The SEC’s decision to withdraw its legal defence is seen as a setback for investors and market participants seeking consistent and comparable climate-related financial information from American companies, but is not necessarily the end of the rules as the rules could still be upheld in the proceedings.

In a similar vein, the US Environmental Protection Agency also announced last month that it would seek to roll back 31 climate, air and water pollution and emissions regulations as part of what it dubbed the “biggest deregulatory action in U.S. history”.

These decisions follow a number of other recent changes in the United States’ approach including its withdrawal from the Paris Agreement, the main global treaty on climate change.

On the flipside, some states are moving ahead with their own climate reporting agenda. California in 2023 adopted laws requiring climate-related corporate disclosures on US companies that meet certain revenue thresholds from 2026. The New York State Department of Environmental Conservation has also recently released draft regulations proposing mandatory greenhouse gas emissions reporting by certain significant emitters, with reporting to begin in 2027. The department is currently seeking public comments on the draft regulations by 1 July 2025.

Canada

In February 2025, Canada's financial regulator, the Office of the Superintendent of Financial Institutions (OSFI), revised the implementation date for Scope 3 emissions reporting for banks and insurance companies to begin in fiscal year 2028, three years later than initially planned. This change aligns with the Canadian Sustainability Standards Board standards, which provide a three-year relief for reporting on Scope 3 emissions.

In addition to extending the timeline for financed emissions reporting, OSFI also revised the implementation date for the disclosure of off-balance sheet emissions starting from fiscal year 2029.

Japan

However, while we have observed delays and withdrawals in some jurisdictions, Japan is an example of a jurisdiction moving ahead with adoption of disclosure standards based on the international sustainability standards.

In March 2025, the Sustainability Standards Board of Japan (SSBJ) announced the release of its finalised inaugural sustainability disclosure standards which are based on the ISSB standards, and anticipated to form the basis of mandatory reporting for listed Japanese companies of sustainability and climate-related information.

The release by the SSBJ includes three standards:

- a universal Sustainability Disclosure Standard Application of the Sustainability Disclosure Standards (application standard);

- a theme-based Sustainability Disclosure Standard No. 1 General Disclosures (general standard); and

- a theme-based Sustainability Disclosure Standard No. 2 Climate-related Disclosures (climate standard).

In doing so, the SSBJ has effectively split the requirements in international sustainability standard IFRS S1 General Requirements for Disclosure of Sustainability- related Financial Information into two standards (i.e. the application standard and the general standard). The requirements in the “core content” section of IFRS S1 have been included in the general standard and the requirements that prescribe the basic requirements for preparing sustainability-related financial disclosures have been included in the application standard.

New Zealand

Meanwhile, New Zealand’s climate-related disclosure regime was introduced in 2021 and similarly requires climate reporting entities to produce annual climate statements developed by the External Reporting Board. It impacts around 170 financial market participants in New Zealand and overseas incorporated organisations where their business meets certain thresholds.

Earlier this year, New Zealand’s Ministry of Business, Innovation and Employment (MBIE) conducted a public consultation on potential adjustments to ensure that reporting thresholds and director liability settings are appropriate and proportionate. This was done in response to stakeholder concerns about the cost and burden associated with reporting. Findings from this consultation are yet to be made public.

This consultation builds on past consultations conducted by MBIE and New Zealand’s Ministry for Environment (MfE) on the future of assurance obligations for climate reporting entities and specifically considered whether there should be an occupational licensing regime for CRD assurance practitioners and whether the scope of the assurance requirement should be extended to assurance over all disclosures made in climate statements. This consultation closed on 10 February 2023 with the MBIE and MfE reported to be analysing submissions to inform future decisions on assurance obligations.

In the meantime, New Zealand’s XRB have approved and issued changes which provide climate reporting entities with an additional year of relief from disclosure and assurance of scope 3 greenhouse gas emissions and anticipated financial impacts disclosures. Climate reporting entities may apply these standards for accounting periods that begin on or after 1 January 2024.

Implications for Australian companies

These regulatory changes and delays overseas highlight the complexity for Australian companies trying to navigate and comply with different regulatory approaches and standards for their overseas operations.

With the weight of momentum moving towards increased climate-related reporting, Australian companies may also benefit from the enhanced transparency and comparability of climate-related information in the global market, as well as from the opportunities to learn from and collaborate with their peers and partners in other jurisdictions. Given the global nature of business and supply chains, these disclosures may also enable Australian companies to more effectively manage climate risks and opportunities.

In Australia, companies expected to be within scope of the mandatory reporting regime should continue preparing on the basis of the law as it stands.